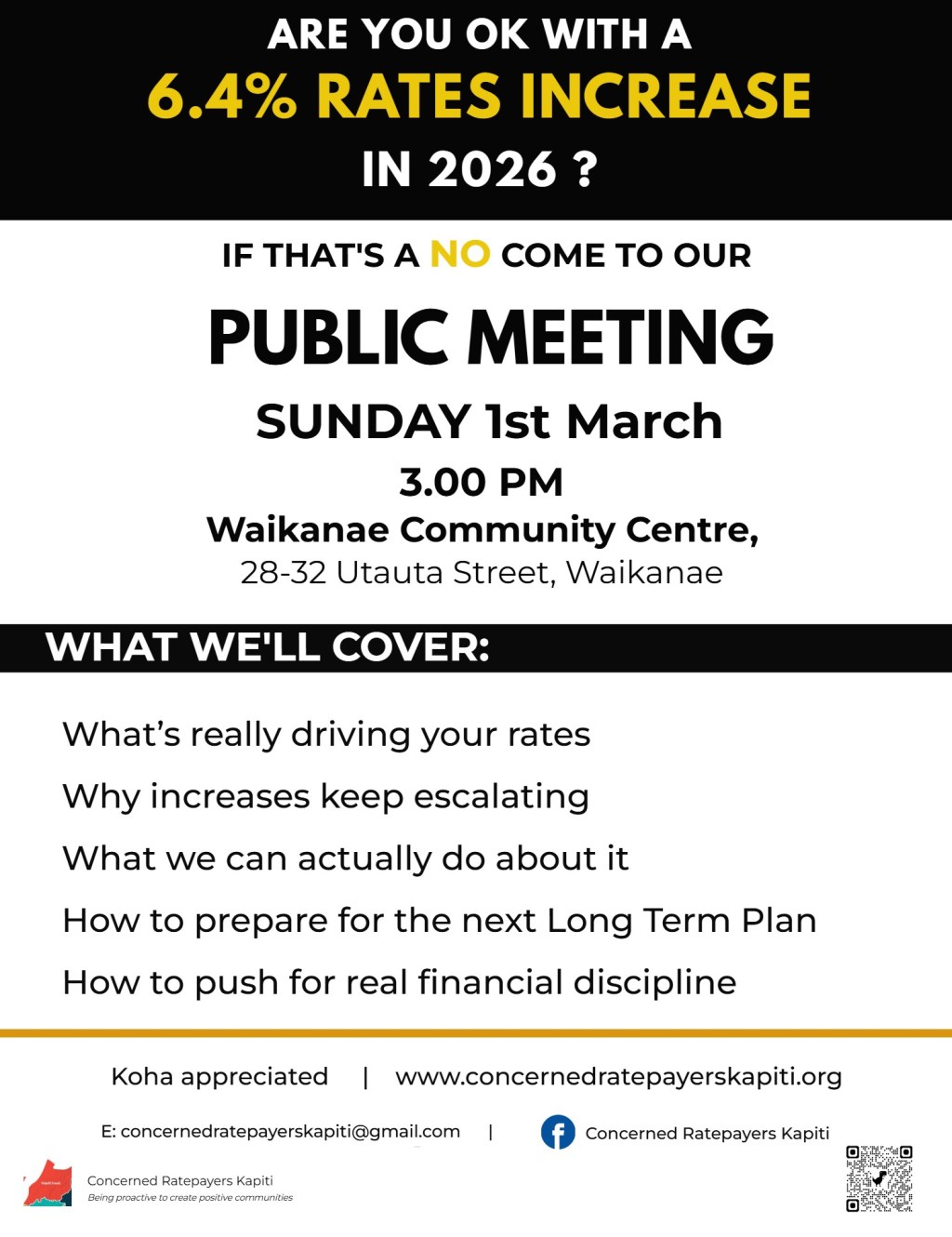

A three-part analysis of the budget system driving Kāpiti’s rates increases

By: Michael Papesch and Kathryn Ennis-Carter, members of the Concerned Ratepayers Kapiti Committee

We have spent our professional lives working on central and local governments’ budget processes, co-ordinating planning and budget bids, and leading reviews to reduce spending. We have also worked on local and central government governance legislation and processes. We have also both undertaken these professional activities internationally, advising other governments. So we have a lot of experience to draw from about what types of budget-setting systems will control costs, and which budgeting systems won’t.

Article Two: The Defence of the System (and why it fails)

In the first of our series about how rates are set in Kapiti, we outlined how the level of rates is really set by this Council. We outlined that it’s a cost-plus system: staff take last years’ budget, add on to it all of the “cost pressures” that you can think of, and hey presto, that’s the starting point for the new financial year. If the resulting increase is considered too high – even for those Councillors who think high rates are okay – then look to make spending cuts through a random list of “low hanging fruit” provided by Council staff. But, importantly, none of the “low hanging fruit” are for costs generated within the Council (other than for a few items that were finishing anyway).

By far the best question at Council Briefing #3 was from Councillor Liz Koh, who asked, seemingly frustratedly: “Are we being funnelled?”. What we think she was getting at was that the process at Briefing #3 was channelling all of the discussion towards cutting spending that she actually cares quite deeply about. But the process seemed designed to inevitably lead towards cutting the items put forward by staff, with no other options on the table.

Respondents at the meeting assured Councillor Koh that she was not being “funnelled.” But it’s pretty clear to any outsider watching the process that the real answer to this question was: “Yes, you are.”

If you missed our first article, no, we are not making this up. You can read the detail of how this process works here. [insert link]

Our second article explores what the supporters of this process might say, and our response to them. Because this process has been going on for a while, there must be something good about it, right?

Defenders of the current Budget process might say that automatically adding “cost pressures” into the base budget is necessary to ensure that core Council services – pipes, parks, pools, and libraries – can continue without service cuts. We have seen this play out in neighbouring Councils such as Wellington City Council …. any modification of what the budget increase that the staff want inevitably means that swimming pools will have to close, beloved community facilities will have to close (remember the Begonia House?) and library hours will have to be cut. Nobody wants to contemplate that. And so the cost-plus approach to budgeting is rarely challenged.

But accepting the cost-plus approach is believing that Council services are already 100% efficient, there is not a single dollar of questionable spending, and no opportunities to re-prioritise spending. Do you believe this is true?

In bureaucracies such as KCDC, there are always ways to deliver with the same or less. We have both managed business units in central government departments and in local councils. In Michael’s case, in his last job before he retired, he thought his budget was already operating on ‘the bones’ and then he found his budget was progressively cut by 25% over six years. He had to cut staff, but by working smarter and focussing on those things that clients really wanted, he was able to keep delivering while increasing his unit’s quality standards.

There is no reason to believe that KCDC staff wouldn’t be able to do the same in their business units.

Business unit managers also know that, in their work programmes, there are the “absolutely must do” items, and the “nice to haves.” In a cost-plus world, you’d be able to do all of them. If it’s not a cost-plus world, commit to the quality delivery of the “absolutely must-do,” and work with your clients to prioritise which of the “nice-to-haves” are the most important.

At a CRK meeting with the Mayor and some Councillors, Kathryn asked whether Council has ever done a review of its activities to identify which are ‘core services’ (i.e. the ‘have to do’ functions) and which are ‘discretionary’ (i.e. the ‘nice to do’). From the response, it was clear that there had not been such an analysis – the Council operates on the basis that everything it is currently doing must continue, and be added to.

It was very striking that the word” re-prioritisation” was never mentioned at Council Briefing #3.

Another thing the defenders of the 2026/27 budget process might argue is that the Council did find savings in its own budget last year, and so their argument is that this process is not as bad as we (CRK) are making out. It is true that a year ago, Council staff offered up cost savings of about $1.9 million (out of total savings of $3.1 million) from Council functions. But that was only after the budget process added $14.2 million to its opening budget – that was the value last year of all the “red bits” in this year’s diagram (see Article one for a copy of the diagram we are talking about). The net increase to the Council’s own budget last year – because of all of the “red bits” – was about $12.3 million. That’s still a cost-plus approach.

Sometimes you hear that local government costs increase faster than the general rate of inflation, and so rates increases above the rate of inflation are simply unavoidable. In an attempt to back up their case, in February 2024, Local Government New Zealand commissioned Infometrics to report on the cost increases faced by local authorities. Infometrics estimated that local government operating costs (the costs funded by rates) increased 19% between 2020 and 2023. But a check of the Reserve Bank inflation calculator shows that general CPI inflation was also 19% between 2020 to 2023. Unfortunately for the defenders of the current budget process, it is an unfortunate truism that they would prefer not to acknowledge, that local government operating costs, and general CPI inflation, track each other quite closely.

Whichever way you look at it, the current approach is good for the Council –their budgets are protected – but is terrible for you, the ratepayer, and for any Councillor wanting to deliver a lower rates path for you.

The good news is that we see rate capping as a key lever to change the current process -it will force KCDC to change if nothing else does. The unfortunate news however, is that rates capping will not come fully into effect until 2029. The Government has advised Councils that they should take the intended rates capping legislation into account when setting rates levels for the 2026/27 and 2027/28 financial years. However, KCDC is behaving as though they didn’t hear this direction. Are they deaf, uninformed, or just plain ignoring it?

That all means that getting a lower rates path demands that Councillors collectively agree to change KCDC’s approach to budgeting and rates setting in Kapiti now. If they don’t change it …. well, if you keep on doing what you always do, you’ll keep on getting what you always got. In our next article, we’ll set out how Councillors can change this process to something that would work better for them and deliver a lower rates path for you.