A three-part analysis of the budget system driving Kāpiti’s rates increases

By: Michael Papesch and Kathryn Ennis-Carter, members of the Concerned Ratepayers Kapiti Committee

We have spent our professional lives working on central and local governments’ budget processes, co-ordinating planning and budget bids, and leading reviews to reduce spending. We have also worked on local and central government governance legislation and processes. We have also both undertaken these professional activities internationally, advising other governments. So we have a lot of experience to draw from about what types of budget-setting systems will control costs, and which budgeting systems won’t.

Article Three: How it can be fixed

Over the last couple of articles in our series about how rates are set in Kapiti, we have outlined how the level of rates is really set by this Council. We outlined that it’s a cost-plus system: take last years’ budget, add onto it all of the “cost pressures” that you can think of, and hey presto, that’s the starting point for the new financial year. If the resulting increase is considered too high – even for those Councillors who have demonstrated a willingness to vote for high rates increases– then KCDC looks to make spending cuts through a random list of “low hanging fruit” provided by Council staff. But, importantly, none of the “low hanging fruit” is for costs generated within the Council (other than for a few items that were finishing anyway). You can find our first article HERE.

We have also outlined what the supporters of this approach might say in its defence, and how those arguments really don’t stack up. You can find this in article 2 HERE

In this, our final article, we set out how this system can be changed now – if enough Councillors want to do so. Because there are better ways to set budgets – that allow for cost control, extra funding for the new goods and services that KCDC wants to deliver – and repay debt.

We will call this the “Clark-Cullen” approach to budget setting.

This is the approach used by Dame Helen Clark and Sir Michael Cullen when they were Prime Minister and Minister of Finance respectively, in the early 2000’s. Those of you old enough may recall they spent on new things such as interest free student loans and KiwiSaver. But they also kept core costs under control and ran surpluses to reduce Government debt.

But, unlike KCDC, the thing they did not do was run a cost-plus approach to budgeting.

The principles use by Clark and Cullen were straightforward – and would be similar to the principles that you would use in your own household or business. Below, we set out how you could apply the “Clark-Cullen” principles to KCDC:

- Set a limit of how much the Council budget can increase in advance of Council staff starting their annual budgeting process. Ideally, this limit would be set for the three years each Council has been elected and would be based on their view of what ratepayers can afford.

If our KCDC Councillors followed through on what they talked about during the election campaign, they would consider the compounding effect of the rates increases they have already voted in for the last three years and set a budget limit of rates increases to about 3% per annum, on average, for the next three years. - Stop the cost-plus pricing approach – that is, stop the automatic incremental increase to the base budget, as a result of adding “cost pressures” to the Council’s own budget, year after year. Stopping an incremental ‘cost-plus’ approach year after year means that some of the “cost pressures” will have to be absorbed by the Council – either by working smarter, finding lower cost suppliers, cutting out some of the activities Council is currently undertaking, and by making cost savings via the ‘low hanging fruit’ approach within the Council itself.

If some of the increases in costs cannot reasonably be absorbed by the Council, then staff should make a business case about why this is so and why this part of the budget should be topped up. But any such increase affecting the core Council budget must come out of the spending limit set in advance in (1) above. - Review the level of operational spending from a first principles perspective. This should have three components to the analysis.

- First, identify those functions which are the core, public-good functions the Council must undertake (pipes for water services, swimming pools, parks, libraries etc). Establish the baseline budget for these.

- Second – conduct a ‘baseline review.’ Review any ‘cost drivers’ that are likely to put up the baseline budget for these activities. Identify any ‘cost drivers’ that can be reduced or can be offset by savings to existing costs. This should be done systematically, rather than via a random list of ‘low-hanging fruit.” Council provided activities should be within scope of a first principles review of such spending.

Cost savings can be identified even for pipes, parks, pools, and libraries. This kind of ‘baseline review’ should be done each year to examine the reality and impact of ‘cost drivers’ for core services. And periodically an external review of the baseline – considering priorities, process efficiency, and procurement to ensure that KCDC is operating as efficiently as it can. - Third, review all the list of ‘discretionary’ activities that Council is currently undertaking.

The first part of the review of these activities should follow the same process as for the ‘baseline review’ outlined above – i.e. looking at ‘cost drivers’ and potential savings.

But all discretionary activities should be reviewed additionally from a ‘first principles’ and ‘public good’ perspective. For example – Is the activity required under, or consistent with, the Local Government Act? Is it a ‘public good’ which benefits or is used by the whole community, or just a section of the community? Who wants this activity? Who benefits? Who pays?

The review of ‘discretionary’ activities should provide Councillors with a clear rationale for continuing the activity, and the level of cost it is adding to the ‘core budget.’

All new initiatives and new spending proposals for ‘discretionary’ activities should be rigorously reviewed, to avoid embedding unnecessary spending into the baseline.

- First, identify those functions which are the core, public-good functions the Council must undertake (pipes for water services, swimming pools, parks, libraries etc). Establish the baseline budget for these.

- Review the level of capital expenditure, which is driving depreciation and interest costs. Depreciation is a very large driver of increases to Council costs. Unlike the scare mongering that you hear when the level of capital spending should be looked at, reviewing the level of capital spending does not necessarily mean cutting back of spending on transport or Three Waters. About $268 million of KCDC’s planned capital spending over the next 10 years is on items other than transport or water services.

This system of budget discipline worked wonders for Dame Helen Clark and Sir Michael Cullen. There is no reason why it cannot be used in Kapiti. It’s simply a question of whether the Councillors will demand it and have the courage to make decisions on the basis of ‘public good’ choices and cut unnecessary spending by cutting out unnecessary activities.

Change to the budget system needs to happen now. Once the rates level for 2026/27 has been set, the Council will start thinking about its next Long-Term Plan. That will set a baseline budget for the next 10 years. The current Long-Term Plan uses the same cost-plus approach that this year’s Annual Plan does. Continuation of that approach will be disastrous for all ratepayers across the region.

The good news is that that our Briefing to the Incoming Council (which you can read HERE) spells out how to design and deliver the “Clark-Cullen” new budget approach. If Councillors didn’t know how to turn around the budget process – so that they get more control over the budget and are able to rein in costs and spending – they do now.

The question now is – Will they do it? If the Councillors find themselves in the same bind next year, they only have themselves to blame. And you – the ratepayers and residents – will continue to pay.

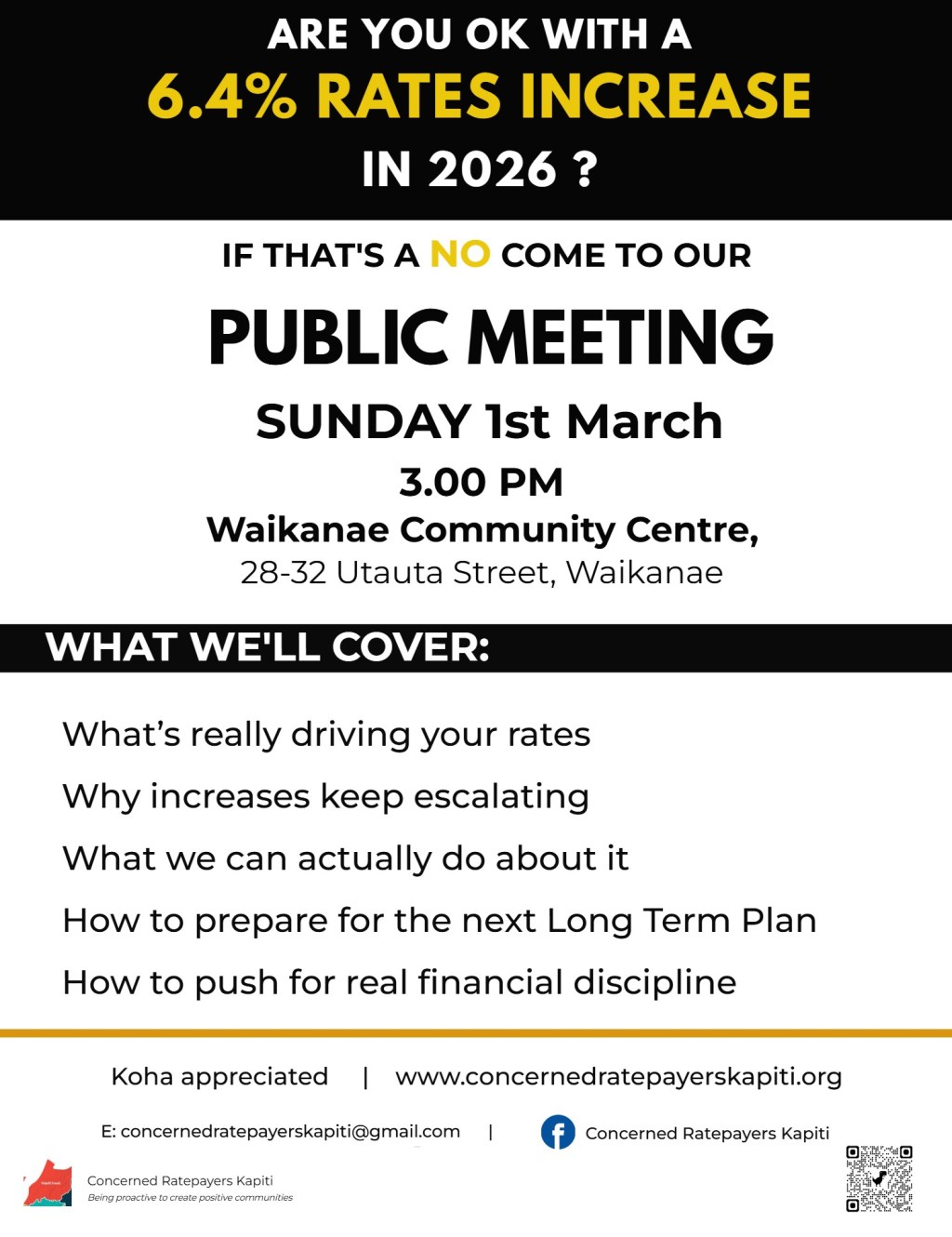

You can help them by writing or emailing them, saying you are unhappy with a rates increase of between 5.7% and 6.4%. We have a template you can use HERE. Or you can come to a public meeting on the upcoming rates increase at 3pm on Sunday 1st of March – details HERE.

Please send or give this article to any of your friends, neighbours or family who are concerned about how they are going to pay their rates. Because the problem can be fixed. And you can help put the pressure on Councillors to make sure it is fixed.